Deep Dive: Biodiversity Credit Sales

All public voluntary biodiversity credit transactions in a single database. Plus a quick analysis.

Hi friends 👋

It’s been a while since I shared any hard data with you. My bad - bigger and better things take more time. Being hopelessly optimistic with timelines doesn’t help either. Just ask my collaborators (hey Joshua 🙃).

I do have a goodie for you though - a database of all public voluntary biodiversity credit transactions I could collect. Most of these are business-to-business (B2B) but I aggregated some business-to-consumer (B2C) ones as well.

This is a subscriber-only special. To access the database, you have to first subscribe to the newsletter. You'll then get the Airtable link in the welcome email. For the existing subscribers, you’ll find the link in the original newsletter in your inbox.

And if you don’t see your transaction in the database (or it is inaccurate), just fill in this form (or ping me personally if you need to share additional context). And thank you to all the credit schemes and project developers who trusted me with their sales numbers. I take that seriously.

Let’s dig in.

Disclaimers

As always, a couple of disclaimers:

This analysis will be based on data from three sources:

publicly available (shared above),

privately shared,

conservative estimates.

Throughout, I’ll be traversing through all three. Confusing but necessary - this is a sensitive topic. The public-only numbers are obviously lower than reality. That’s also why you won’t see every transaction in the public database. It is the majority though.

The definition of a biodiversity/nature credit is still undefined in practice. I’ll use a relatively wide interpretation of it (or at least wider than Pollination). As an indirect result of that, many purchases aren’t “pure” biodiversity credit purchases. They might be stapled to carbon credits or include other ecosystem services in the project area.

Not every transaction listed is a purchase. A couple of them are also pilot investments, pre-purchases or commitments to purchase. Most of them probably aren’t that large though.

Not everything here is accurate. Easily accessible market data is not the luxury we have. I’m sure I missed some B2C sales since not everyone shares them publicly.

The sales numbers in the original article have been slightly adjusted with the most recent credit sales data.

Analysis

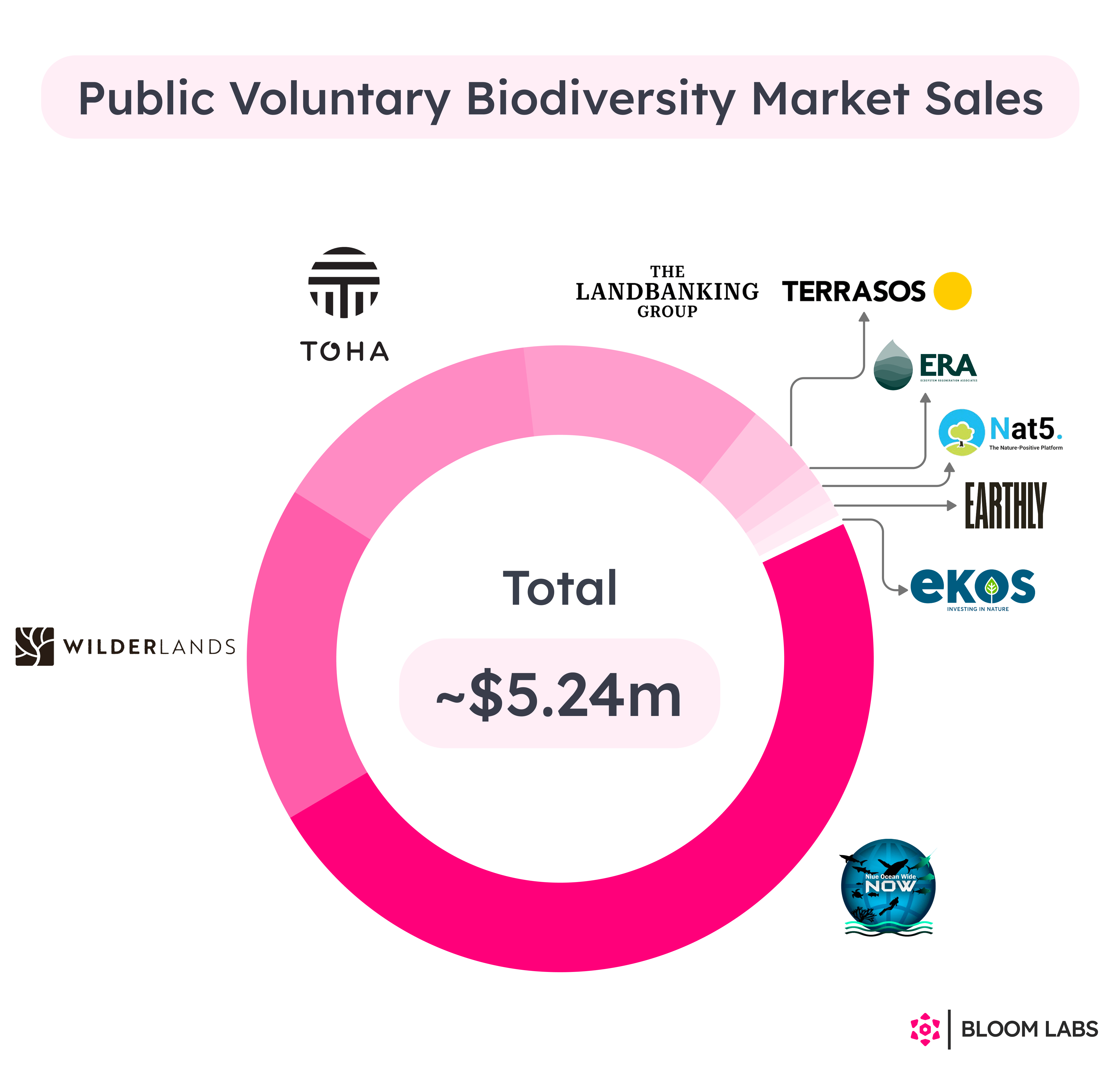

Sales totals and leaders

No matter how you cut it, B2B sales dominate. They do stand on a couple of large public sales though:

Niue’s ~NZD 4.5 million credit sales, with 80%+ of it coming from organizations, not individuals.

The Landbanking Group’s three 6-figure sales.

Wilderlands’ 70,000 credits sold in 5 weeks, probably worth anywhere from $140k to $490k.

These four alone make up 90%+(!!!) of the total sales. Oceanians are running the game early on - just take a look below.

Area

The total area protected or restored is ~1,727,750ha, or ~17,278km2. Without the Niue Ocean Wide Trust, it’s ~27,750ha. And the remaining area is mostly composed of The Landbanking Group’s year-long conservation agreements (20,200ha).

In other words, the current voluntary biodiversity market’s area-based impact is a drop in the ocean, given our global goals.

Geography

The majority of buyers purchased credits from the projects in their main country of operations. The exceptions came from European and North American companies, some of whom also supported South American projects. No surprises here, given how important locality is for biodiversity credit buyers.

Indigenous-led leads

Niue Ocean Wide Trust, Toha Network and Savimbo are some of the early market leaders (with EarthAcre seemingly doing just as well). And they’re all Indigenous-led. It’s a signal of confidence that the right thing is being rewarded.

Buyers

The Western buyers dominate with only 3 out of 23 public B2B transactions led by non-Western countries (Mexico, Colombia and Brazil). Most seem to be test purchases.

There are no obvious buyer industry trends. Industries range from manufacturing, healthcare, banking or luxury goods to tech, personal care or even NGOs.

Even though 19 out of known B2B 23 transactions are led by for-profit players, contribution-based/philanthropic motivations are the dominant demand drivers.

SME buyers lead the pack

Small/medium businesses are the buyers ~80% of the time.

That makes sense. There’s less bureaucracy required to get internal approval to buy. Buyers don’t need (or have to hide behind) a company-wide nature strategy. Often, they are founder-led and buy simply because they believe it’s the right thing to do. For now, still a very philanthropic marketing-y approach. Of course, the purchase amounts are usually more modest as well.

Some corporates engage but often indirectly

We also have 9 documented corporate (250+ employees) transactions. Not all of them are direct though. For example, the Sun Institute Environment and Sustainability, purchaser of The Landbanking Group’s VNUs, was established by the Deutsche Post Foundation in 2014 (which in itself is a separate entity from the $40b+ giant). Another example: Microsoft’s recent funding for a local non-profit to buy some biodiversity credits near one of their data centers in Sweden. And the last one: Air New Zealand. They purchased Toha Network’s MAHI tokens via its Climate and Nature Fund. The whole transaction itself was unique, with access to data being a big buying motivation (for their corporate disclosures). MAHI tokens aren’t your traditional biodiversity credits either.

Corporate purchases can be difficult to approve. Purchasing indirectly can skip some of these bureaucratic hurdles.

Preservation dominates

70%+ of the projects are for preservation. The remaining: restoration, sustainable use or a combination of these with preservation. No big surprise here - the preservation credits usually take the least time to issue and are the cheapest conservation projects to start.

Unspecified claims

Most buyers don’t yet make any claims using their purchased credits. Those who do, usually make contribution claims. Few buyers connect their own product sales with credit sales (e.g. “each festival ticket you buy will preserve 1m2 of Australian native habitat forever”). Only one pre-purchaser (Mexican investment firm LGL Investments) specified profit as the main reason to purchase.

Either way, the claims that can be made aren’t well-defined yet. That’s why most buyers will probably avoid risking their brand with any bold claims, taught by the carbon controversies. The market needs a widely accepted biodiversity claims guidance.

Here’s an interesting fact though - no one used voluntary biodiversity credits for offsetting yet. Zero. Voluntary credit accounting is still so unclear and unstandardized that no buyer has yet taken a risk to make any compensatory claims. I’m very curious how the credit schemes that do support some level of offsetting will do this year (e.g. 3Bee, Botanic Gardens Conservation International, Bluebell Index or LIFE Institute).

Why aren’t there more transactions?

The million-dollar question. One can easily name 10+ reasons. I’ll focus on a couple of the most important ones in my experience:

1. Lack of standardization & credibility

The voluntary biodiversity market (VBM) is both early and (at least a little) more complex than any other environmental market. Not a great combination if one expects big voluntary buyers to line up fast.

The high-level market principles are just forming right now, with many disagreements remaining. We still don’t have any real monitoring-related guidance (although ecosystem condition is becoming the dominant high-level framework). We still don’t have any agreed upon biodiversity units, nor might we ever have them. We still don’t have unified claims guidance (although schemes like NaturePlus™ or CreditNature have thought about it deeply). We still don’t really know how well the biodiversity credit metrics will play with the upcoming nature accounting (mainly CSRD & TNFD) reports. We still have a patchy and divided stance on the crucial technicalities like additionality, durability, tradability or benefit sharing. On top of that, new biodiversity credit schemes with their own unique rules are still being baked, although at a slower place.

With all that, I’m aware that this young market needs some breathing room with less standardization (i.e. restrictions) for at least a little bit. There are still some things we don’t understand. And we can’t put rules on things we don’t understand.

The perpetual affliction

One must also admit that the market’s voluntary nature will always be a problem in standardizing the market and convincing the buyers. The space might need a “benevolent dictator” to actually move things forward. It could be a big buyer or, ironically, a big government. Either way, only someone with enough influence could pull this off and handle the inevitable criticism.

2. Unclear business case

For-profits prioritize (short-term) profit. That’s the way it is for now.

Unlike voluntary carbon credits, the biodiversity ones are currently limited to contributions as the primary demand driver. Offsetting is not yet in the picture (although it’s probably a must if the voluntary market is to reach any meaningful scale). Not yet having corporate nature targets doesn’t help either. There’s progress on all target-setting fronts though: corporate, national and international.

We could also look into the financial benefits of improving ecosystems that businesses and governments rely on. What we do know is that 1. they exist 2. most aren’t yet properly quantifiable nor predictable 3. they take time. I believe the third is the deal-breaker for most for-profits. Why care about returns in 10-50 years if you are rewarded annually? Either way, nature is closer to real economies than carbon. That’s why I hope that the increasing pressure on ecosystems and technological improvements will lead to ways of valuing nature better.

Public goods and private money can be a horrible combination. The natural response of investors is to privatize the public goods. That’s the surest way to get their return. That cannot always happen though - some goods are meant to be public. Fresh water, clean air, healthy soils, biodiversity, you name it.

3. Early market sales take time

This might sound like a cop-out answer for some but we should remember one of the first lessons in sales - the bigger the sale, the more time it takes. And quite a couple of schemes believe they are close to finalizing larger transactions. They and the schemes that may have even sold already may not be incentivized to share much for competitive reasons. Now, keeping that private for long only makes sense if the buyer hasn’t done their due diligence on other schemes and might start comparing their current vendor with 50+ other choices. They might even decide that they might have overpaid. Early markets allow for price discrimination.

And finally, credit validation, verification and issuance takes time. Years, to be exact. Most projects started in 2023 aren’t yet eligible for credit issuance, especially the very popular restoration ones. That’s why most of the credits sold aren’t yet certified.

Pioneer buyers

So, the market is risky and doesn’t promise immediate returns. Easy reasons for corporates to justify not buying. Just like every early market, VBM requires pioneer buyers. These won’t be the organizations buying only for direct profit (philanthropies, you can still step up!). For the market to reach any meaningful scale though, companies will need to start seeing profit sooner or later. Ideally directly (reduced nature risk/insetting, speculation) but also indirectly (increased brand value).

More musings

B2B vs B2C sales

At least publicly, B2B sales make up ~80% of the total. In my opinion, similar to carbon, B2C sales might increase but will never be meaningful. The current ~20% might be the highest proportion of total sales it will ever have. Only relying on people’s good hearts (and them understanding biodiversity credits) is a strategy built on hope. Plus, it’s not always easy to even buy these credits as an individual.

The risks

I’m seeing two worrying trends right now:

The endless risk of greenwashing

The classic criticism against environmental credits is that corporate credit buyers might use these purchases to greenwash and/or stall the real regulations.

Well, the previously mentioned biodiversity credit buyer, SUN Institute Environment & Sustainability, was established by the Deutsche Post Foundation which itself was established by the Deutsche Post DHL Group. The CFO of the latter called for a stop to work on sector-specific CSRD’s European Sustainability Reporting Standards (ESRS) - bad for nature. It’s a reach to connect these but it’s an example of what we should avoid.

Another example: last year, Air New Zealand dropped their 2030 emissions target and pulled out of the Science Based Targets Initiative (SBTi).

Private funding replacing public funding?

The biodiversity credit project that Microsoft has recently supported looks like a direct response to the project’s loss of public funding. Private nature finance must increase but it cannot replace its public counterpart. Public nature funding is the most reliable long-term solution for much of the non-commercial conservation. There’s no way around it. Of course, the multi-decadal weakening of the public sector in the West and the current geopolitical situation might force many conservationists to rely on the private sector instead, at least for now.

Although these are just single data points, we shouldn’t ignore them.

The start of something

As unique as the voluntary biodiversity market is, it follows the same old market cycles. A bunch of ecstatic hopefulness followed by just as cynical hopelessness, on repeat. A great testing ground for the compliance markets which will inevitably be (and already are, for decades) much larger.

One thing is certain though, these markets reflect a different way of thinking about nature, whether good or bad (hopefully good!). This “nature + market” tool isn’t going away any time soon either. We’re at the start of a megatrend: increasing pressure on ecosystems, increasing costs of ignoring nature and increasing economies combined with limited natural resources are leading us to a breaking point. I’m done trying to predict when. But acknowledging that and working to do something for nature is what matters in my opinion. Either way, this megatrend will make sure our economies don’t ignore nature for much longer. Exciting times.

Related reads

Weekly OPIS Biodiversity Market Reports. Quick and valuable pieces that feature project-level pricing for some biodiversity credit schemes. Top-notch stuff.

Pollination’s report on voluntary biodiversity credit markets. Pollination folks never disappoint. There they also shared a realistic market size estimate in 2024.

A student here trying to navigate the complex and ever-evolving landscape... this is insanely helpful. Thank you so much for the amazing work!

Great insights Simas!! I appreciate the perfect balance you are striking between free and paywalled content, and wishing you enormous success!!