Biodiversity Credits: For & Against

A collection of all main pro and anti arguments for biodiversity credits

Today’s piece is brought to you by some of my favorite people - the folks behind Planet Wild.

Planet Wild is a nature conservation organization that uses the power of community to protect biodiversity worldwide.

Its community consists of ordinary people (& companies!) who crowdfund pioneering biodiversity projects that save animals, oceans & forests. All you need to do is choose a monthly/yearly contribution and see how your money is used to fund a new project every month on YouTube. That’s what I do.

Seeing the immediate impact your contribution has is what makes it genius to me. We need more beautiful nature recovery stories.

Consider following me and becoming and member as well. As a special welcome, I offer you the first month for free with the code SIMAS9 here.

Companies are also very welcome to team up with Planet Wild! Just ping partner@planetwild.com and tell them Simas has sent you.

Hi friends 👋

I see in grey. No, I’m not color-blind (I think?). But I’m rarely categorical in life. Usually, I’m the “it depends” guy. Same with biodiversity credits. I fell in love with them.. for about a month. Then the romance became less romance-y.

Almost two years in, I should probably give you a glimpse of what’s happening in my brain on a daily. Time to explore the main arguments that biodiversity credit supporters and critics use. My experience at COP16 and the house of bubbles I saw made me prioritize this piece.

This was more (and more fun) than I expected.

Let’s get to it.

Biodiversity Credits: For & Against

(Click the link 👆 to read the full Deep Dive online)

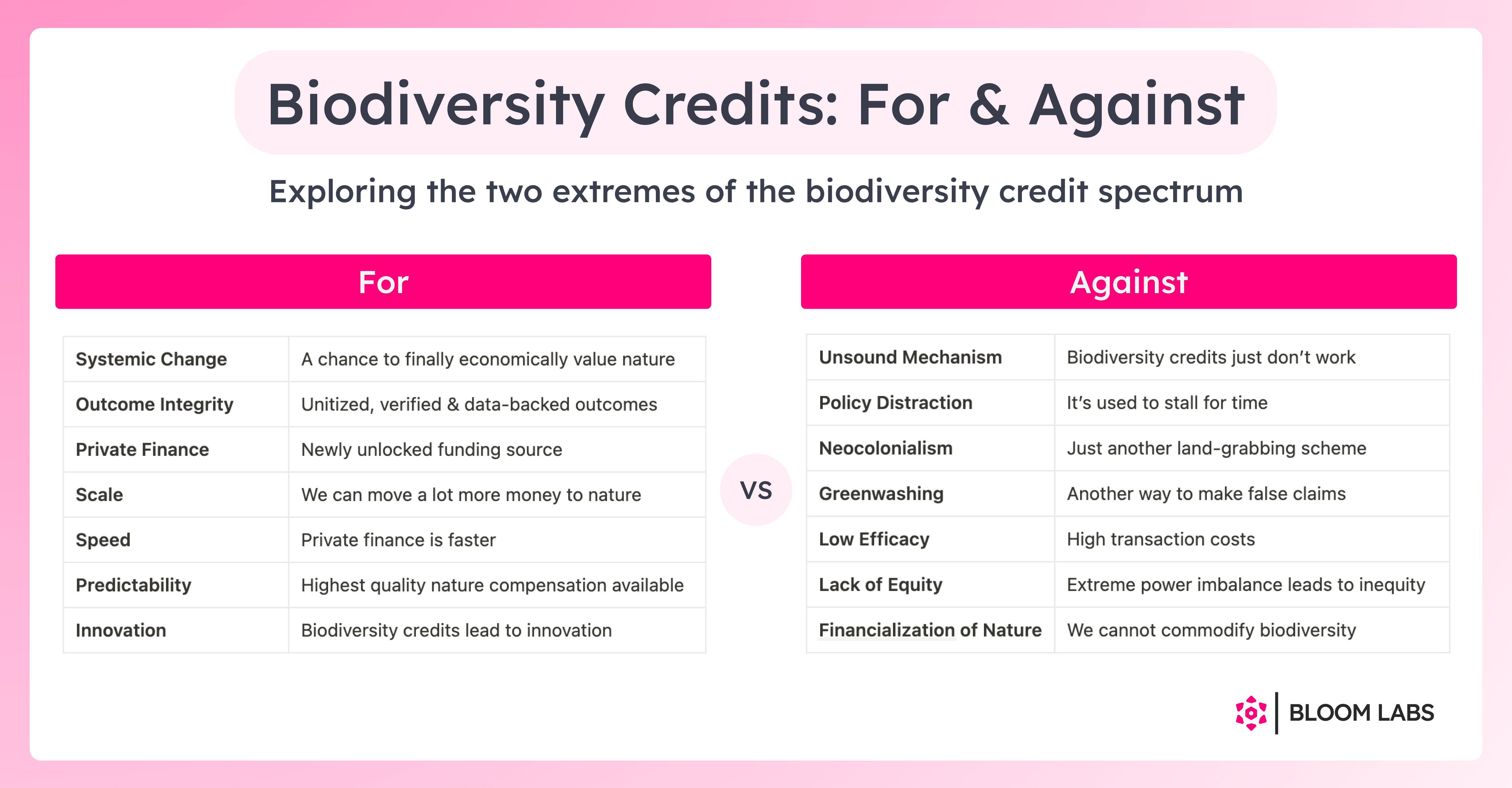

The pro biodiversity credit perspective

Biodiversity credits is a significant step forward in how we value and finance nature. They enable buyers to pay for truly demonstrable, transparent and verified nature outcomes. They allow us to finally represent nature on our balance sheets and give it a real value instead of 0. Additionally, the merging of nature and financial accounting through a set of standardized nature units leads to a high integrity nature monitoring system. And with higher integrity, comes higher trust. That will finally allow us to ensure high-quality, additional, leakage-free and durable nature and social outcomes where in the past, we were in the dark. And most importantly, we will be able to do so at scale. Biodiversity credits might even be used to tackle commercial nature risks for corporates within and near their value chains.

These markets are built with people at the front and center. The primary purpose of biodiversity credits is to improve the lives of local nature stewards. That can only happen by working together with them, respecting their rights and, ideally, them (co-)leading these biodiversity credit efforts.

The systemic nature of markets makes it a high-risk and high-reward solution. That’s why biodiversity credit markets must be well-designed from the beginning, with transparency and accountability in mind. And that’s what the market is doing by establishing best practices around nature outcome verification, social equity and market governance.

Now, are markets the perfect solution to our problems? Not at all. But we need more environmental solutions and we need them yesterday. In an ideal world, unified international policy agreements and ambitious national regulations would lead nature action. However, we can’t only rely on governments to lead this global movement - the ever-changing political climate prevents that from happening. That’s why markets should be part of the solution mix to internalize the externalities on time. Biodiversity credits provide a viable way to do just that at scale and by finally involving the private sector - a stakeholder historically over-involved in nature degradation but under-involved in its conservation. Here the governments should develop and enforce clear rules and provide guarantees to involve the private sector at scale. That’s how a well-functioning society works - the government sets the rules and the private sector follows them to achieve the desired outcomes.

With that in mind, biodiversity credits cannot be a substitute for more consistent nature protection policies. Nor can it be a substitute for public and multi-lateral finance. These credits have great potential but are just a tool in a toolbox.

One might say that “financializing” nature is just a sophisticated way to legitimize nature destruction. However, life is all about incentives. And unless we provide economic incentives to conserve nature, it will not be conserved. We have to be realistic and consider how economies actually operate - every nation tries to increase the quality of life of their citizens by producing and consuming more. Whether biodiversity credits (and offsetting) exist or not, past experience shows that resources will be plundered anyway. Cities, farms and factories need land and resources to operate. The best we can do is to showcase the immediate economic value of nature and provide companies and governments with scalable high integrity incentives to preserve and restore it.

So, whether we like it or not, with ever-decreasing natural resources and ever-increasing negative impacts of nature degradation on the economies, different nature markets are bound to form anyway. And everything that can be measured, will be measured and be put into a certain unitized economic value eventually. What we should do is learn from past lessons (e.g. in carbon markets) and ensure that we actually deliver nature outcomes by building a high integrity biodiversity credit market from the start.

Sounds familiar? This is my best pro-biodiversity credits impression. Let’s move into the specific arguments and their counterarguments:

Systemic change

Argument

By helping to integrate nature into the balance sheet, biodiversity credits represent a vision where we properly value nature. We could use it as a financial asset with incentives to conserve nature in order to increase its financial value. It could also assist governments in making nature-related decisions.

Although you can manage what you can’t measure, being able to measure it helps. And we are able to measure nature outcomes with biodiversity credits. To account for nature, we must use it in financial accounting.

Counterargument

Systemic change through biodiversity credits is not realistic. The main financial incentive of every for-profit corporation is to grow. That growth happens by increasing production and consumption. Production and consumption inevitably lead to nature degradation. That’s why in practice, companies will never be incentivized to truly conserve nature. The only way to achieve progress here is through regulations.

Outcome integrity

Argument

Unitized, verified and scientifically-valid outcomes can be way higher integrity than what currently exists in the nature conservation industry. Currently, we have no widely adopted unitized nature or impact measurement frameworks to verify nature outcomes. By building a set of standardized measurement protocols and performance-based units of biodiversity gain or avoided loss, we’re ensuring that outcomes are real, additional, leakage-free and permanent.

That’s why, even if biodiversity credits aren’t fully integrated into financial accounting, they can still improve (& hence grow) outcome-based philanthropy - a space that is troubled by highly inconsistent and lower-quality impact measurement systems that inevitably lead to subpar nature outcomes.

Counterargument

There is still no proof that biodiversity credits can actually improve the nature outcome integrity in practice and at scale. The history of compliance biodiversity markets is full of non-compliance and non-delivery. However, all the excitement about the credits built on standardized metrics being able to increase outcome integrity is unhelpful in actually achieving these nature outcomes, which are highly contextual.

Private finance

Argument

Historically, the public sector has dominated nature finance. However, public money is slow, often less reliable and, with current global political circumstances, is just simply not enough. That’s why it’s unreasonable to rely only on public finance to solve the biodiversity loss crisis. The private sector must finally meaningfully contribute to the equation. Biodiversity credits represent a way to attract such private finance for multiple reasons: corporate contributions to global biodiversity goals, local negative impact compensation, nature risk mitigation and more.

Counterargument

Private finance only appears when there is money to be made. When there is a “return on investment”. Since nature is too complex to predictably model (at least for now), we are bound to end up in a speculative market bubble caused by the private sector’s profit-seeking incentives. Although not ideal, public funding and, most importantly, regulations are the two most predictable solutions to the environmental crisis.

And the “insufficient” public funds argument is built on false assumptions. Firstly, it’s a (negative) sign of the private sector’s growth in power at the expense of the public sector. And secondly, the so-called ~$700b nature finance gap could easily be bridged by redirecting just a small part of tax revenue by the largest economies in the world. Let’s remember - the global GDP is over $100t.

Scale

Argument

The unitization of nature is the ultimate form of standardization that enables the complete integration of nature accounting with financial accounting. When we consider nature in every financial decision, that’s when we can systematically move way more capital into nature conservation, finally co-led by the private sector.

Counterargument

The unitization of nature is impossible. If we still push hard enough to agree on a unit or set of units, we are bound to miss crucial aspects that regulate ecosystems and will assign a faulty value to nature. Nature is unquantifiable. And since the topic of biodiversity credits is so divisive, any meaningful scale is not likely - that will negatively affect both the early biodiversity credit suppliers and buyers.

On top of that, even if nature was (incorrectly) unitized, it wouldn’t be widely adopted. Corporates just don’t think in standardized nature units. They consider nature in financial decisions way more contextually and require a custom approach. Biodiversity credits do not offer such flexibility.

Speed

Argument

Public finance is notoriously slow. Project-based grant-making often takes up the majority of a conservation NGO’s efforts.

However, since we are under such immense time pressure to mitigate and adapt to the biodiversity loss crisis, every minute counts. That’s why we need private finance - a more nimble and efficient way to channel larger amounts of capital. More private finance also leads to technical and financial innovation that could help scale the conservation efforts.

Counterargument

Private finance is indeed faster but at what cost? Usually, it truly moves fast only when there is an attractive opportunity to make money. Many ecosystems that need to be preserved and restored do not offer such attractive opportunities.

Predictability

Argument

Biodiversity credits can be a great compensatory mechanism that brings specificity, equivalency and predictability to compensation purchases. Since credits can directly link the damage with the offset or net gain (e.g. local-to-local and like-for-like), it offers the highest quality compensation available. That offers the credit buyers the strongest monetary incentives to avoid and minimize nature degradation.

Counterargument

This use case is built on offsetting, which is an illegitimate and proven non-solution. Again, strict environmental regulation through mechanisms like taxes and public nature finance is the answer. Plus, the strongest incentives to avoid and minimize nature degradation will always come from regulations.

Innovation

Argument

The excitement behind biodiversity credits contributes to an unprecedented wave of technological and financial nature innovation. Many biodiversity monitoring startups plan to rely on biodiversity credit revenue (either by direct credit sales or by supporting credit project developers). At the same time, new financial vehicles are being built for both voluntary and compliance biodiversity markets. Voluntary biodiversity credits is also a great testing ground for new methodologies before entering the compliance markets.

Whatever the end outcome of biodiversity credits will be, it’s difficult to deny that it is leading to general-purpose innovation that will positively impact nature conservation.

Counterargument

The increased international focus on biodiversity is leading to innovation in nature conservation, not biodiversity credits. 2022’s Global Biodiversity Framework (GBF) together with nature accounting frameworks such as CSRD, TNFD or SBTN are leading this innovation. Although speculation around biodiversity credits also leads to new solutions, most of them are by definition ineffective.

The anti biodiversity credit perspective

Biodiversity credits sound great on paper. Who wouldn’t want a mechanism that dramatically increases nature finance while ensuring better outcomes with more confidence? The reality is different. Biodiversity credits is a tool with a patchy history that poses a threat to true nature and social progress.

First of all, environmental crediting systems is just not a sound financial mechanism. It’s highly manipulable with difficult to prove additional outcomes. Our inability to predictably measure nature, an exceptionally strong social component in such credit projects and cost-minimizing market forces compound the structural problems of crediting systems.

Second of all, biodiversity credits can be and are used as a distraction to stall meaningful international nature policy progress. They also risk becoming another land-grabbing mechanism by not only giving a license to destroy nature but also by disempowering the Indigenous Peoples and local communities by restricting their access to land through biodiversity credit projects. Additionally, it enables companies to continue greenwashing while further plundering nature and delaying their own operational impact minimization.

And finally, setting up the biodiversity credit market infrastructure is expensive work. What percentage of the total funds would actually reach the ground and what percentage would go to the intermediaries? The environmental market history here is not promising.

By treating biodiversity as a financial asset, we risk simplifying the complex intrinsic value of ecosystems into mere economic terms. That will inevitably lead to unintended negative consequences. Many problems that biodiversity credits target are not financial - they are social. Which means we need social solutions instead.

The most likely outcome that the biodiversity credits will achieve is further satisfying corporate greed. Instead, we should focus on more effective proven mechanisms to conserve nature, led by ambitious nature policy and regulations.

And that’s the counter perspective. Again, let’s look into some core arguments and counterarguments:

Unsound financial mechanism

Argument

Environmental markets is a fundamentally flawed financial mechanism.

The system is easily gamed via counterfactual and baseline manipulation to prove that these nature outcomes would not have been achieved otherwise (i.e. prove additionality). It’s also challenging to control for leakage - the unintended displacement of negative nature impacts elsewhere as a result of such biodiversity credit projects. On top of that, most credit projects last 20 to 30 years. That is not enough to ensure long-term nature conservation. The hefty crediting system transaction costs make the mechanism even less practical.

Market forces magnify all of the problems mentioned above. For-profit project developers are incentivized to overstate expected outcomes and minimize their costs - which usually means less investment on the ground. Additionally, the potential to create a credit project disincentivizes the landowners to protect their land. Instead, they are incentivized to overstate the risk of nature degradation to prove additionality. Not only does that lead to ineffective land conservation but also to internal social conflicts.

Biodiversity credit projects also face unique project design difficulties. Unlike carbon, it is extremely difficult to design a modelable and durable biodiversity asset. Our science simply isn’t there yet and all the current credit methodologies that attempt to quantify biodiversity are overly-simplistic. And finally, there’s such a strong social component in biodiversity credit projects (so much of it is about changing the habits of local communities), making it impossible to guarantee the intended project outcomes.

Instead, we should focus on more effective nature conservation mechanisms, such as nature and climate focused corporate taxes.

Counterargument

Environmental markets are imperfect (but improving) ways to reflect real world economies and should be respected as such. No nature-focused financial mechanism has been able to perfectly achieve its outcomes. That doesn’t mean we should throw the baby out with the bathwater. Instead, we should acknowledge the progress we’ve made in internalizing externalities and continue improving. We have examples of functioning biodiversity markets that have delivered real and additional ecological gains, such as in the United States or Colombia.

Protected land regulations and corporate taxes alone are not reliable tools to fight the biodiversity loss crisis in a world where everyone wants to improve their material life. Unlike many other systems, crediting mechanisms take into account the opportunity costs of land. It is difficult to expect to permanently protect more ecosystems without periodically re-evaluating their economic value under different land uses. Otherwise, we would end up in a world where, generally, the majority of intact ecosystems in Global South are protected and people aren’t free to develop economically while in the Global North the proportion of protected lands would be way smaller, simply because more lands are already permanently impacted.

The environmental markets are improving across all the challenges mentioned. Better science, better & more unified governance, standardization and nature technology improvements all tackle additionality, leakage, permanence and perverse private sector market-based incentives.

Distraction from policy action

Argument

If the companies responsible for biodiversity loss will use credits to indirectly lobby for less ambitious nature policies or buy them instead of (not in addition to) their own impact reduction, biodiversity credits are net negative.

Actually, we have already seen that at COP16. The EU, together with some developing countries, have successfully blocked the progress of reaching an agreement on funding for the Global Biodiversity Framework (GBF). Instead, they were pushing the "financing from all sources" narrative which is connected to private markets (i.e. biodiversity credits).

An optimist might say that the EU sees more potential in scaling global nature finance flows through private markets. The more realistic scenario is that the EU is attempting to absolve itself from direct international biodiversity funding responsibilities. That is jeopardizing the entire GBF.

Counterargument

First of all, biodiversity credits is designed as an additional nature finance tool that does not replace ambitious policy. Here we could also apply the mitigation hierarchy to policy action. Just like avoiding and minimizing impacts is the most important part in the corporate world, so is policy leadership in international nature action.

Second of all, we don’t yet have convincing evidence that companies use environmental credits to lobby for less environmental regulation. Instead, there is evidence that companies who buy carbon credits decarbonize faster than their sector peers*. It’s reasonable to assume that the same will be the case with biodiversity credits. Designed well, environmental credit systems can act as a useful lever to increase nature finance in addition to internal impact avoidance and minimization among corporates.

Third of all, we should be realistic about what would happen without biodiversity credits. One thing is certain - the rate of nature degradation would not decrease. In fact, the default outcome of degrading nature is that the harm is ignored. Hence it’s unfair to lay a lot of the blame on companies’ inaction on private markets and environmental credits.

And finally, although in an ideal world, nature conservation would be solely led by governments, the reality is different. The government and NGO model of conserving nature has had limited success. Unless we directly involve the actors degrading nature (i.e. companies) and provide them with both positive and negative incentives to conserve it, it’s difficult to expect for biodiversity loss to stop.

*To which a critic might say “all such claims have been debunked here.“

Neocolonialism & land-grabbing

Argument

The industrialized world has a dark past of using obscure mechanisms to get control of more land. Biodiversity credits might become the newest mechanism to result in that. It does so in two ways: by giving the credit buyers a social license to further destroy nature (via offsetting) and by restricting the Indigenous Peoples and local communities from fully accessing the biodiversity credit project’s land resources.

Some might say that biodiversity credits will be used only for contributions to nature without equating them to any nature degradation. But what have we seen so far? Limited corporate demand and an increasing pressure to add offsetting as a use case for these credits, both at the voluntary and compliance markets. Most corporates understand the value of offsetting but don’t understand the value of contributory claims.

Another threat of neocolonialism is biodiversity credit secondary markets. Although the main biodiversity credit forums are formally against international offsetting and secondary markets, they claim that they cannot prevent such activities. Secondary markets will likely lead to speculative credit bubbles that usually only reward the intermediaries instead of local nature stewards.

Counterargument

Neocolonialism and land-grabbing is indeed a big risk. However, it all comes back to credit system design. This criticism is built on the worst possible and unintended consequences of biodiversity credits.

Firstly, these credits do not give a social license to pollute. If some companies end up attempting to do just that, that’s an example of misused biodiversity credits and an ineffective crediting system.

Secondly, biodiversity credit projects must never be imposed on the local populations. Project developers must reach a proper free, prior and informed consent (FPIC) before starting any project. Indigenous Peoples and local communities must always have the right to reject any biodiversity credit projects from being developed in their territories. The local nature stewards must be included in every aspect of project design and delivery and should ideally (co-)lead such projects themselves.

With regard to offsetting, not everyone in the biodiversity credit camp supports it. That is totally justifiable. But we should once again be rational about what would happen without biodiversity credit offsetting. Nature degradation would continue. If offsetting becomes established and is done right (i.e. local-to-local and like-for-like with strong governance, transparency and compliance enforcement), it will reflect (part of) the cost of destroying nature where otherwise that cost wouldn’t have existed. The end outcome would still be better than the status quo now. What matters is that mitigation hierarchy is followed. Companies who first avoid, minimize and restore nature internally before buying credits to contribute to global goals or offset their unmitigated impacts are the companies who use these credits correctly. Appropriate biodiversity credit usage should be enforced.

With regard to secondary markets, the main industry forums are against it. At the moment, biodiversity credit markets resemble projecting financing markets instead of liquid commodity markets (e.g. soy or corn). Instead, the more likely short-term outcome is multiple local markets. That minimizes the risk of intermediary profiteering through secondary markets. Secondary markets might be possible in the future once we progress on nature measurement and align on a single or set of high integrity measurement approaches. If designed well, secondary trading should lead to a more efficient, liquid and cost-effective (hence larger and more impactful) market.

Greenwashing

Argument

Biodiversity credits are likely to lead to potentially misleading corporate claims (e.g. “we’re nature positive”) while globally, the biodiversity loss crisis worsens. It’s especially problematic because there is no global and quantifiable definition of “nature positive” yet. That opens the door for companies to interpret the definition liberally and make inaccurate claims.

Counterargument

Greenwashing is a murky concept. It happens when a company claims to have fewer negative and more positive impacts on nature and society than it actually does. Biodiversity credits is just one of many methods to greenwash. Once again, if designed well, biodiversity credits should never lead to such scandals. In the corporate claims world, biodiversity credits is a tool to achieve additional, quantified and cost-effective positive nature outcomes after all negative impacts have been reduced within company value chains. In other words, if the mitigation hierarchy is followed correctly, biodiversity credits do not pose a greenwashing risk. Additionally, the quantifiable definition of “nature positive” is being developed at this very moment.

And, ideally, the governments would develop and enforce rules on biodiversity credit claims and reporting.

Low efficacy

Argument

Setting up an environmental market infrastructure is complicated and expensive, often costing the projects a quarter to a half of the total funds. Each market participant (e.g. project developer, MRV provider, marketplace, trader, broker, credit ratings agency, etc.) demands its cut. Such systems are expensive because of the attempts to address the inherent integrity holes of crediting mechanisms (e.g. additionality, permanence, leakage). And for-profit companies usually have even higher transaction costs to justify their profit-making status. Additionally, biodiversity is difficult to quantify, which will likely make it an even more expensive and less efficient market.

Counterargument

Every market infrastructure requires additional costs. Biodiversity credit markets are no different. However, these markets have the opportunity to unlock the scale of private finance not seen before. That should compensate for the low market efficacy at the early stages. We must be patient with many upfront investments and ongoing costs required to build a high-quality nature market. However, once we do, the low efficacy problem should be solved.

High integrity requires additional costs. However, high integrity leads to higher trust. And higher trust leads to higher scale. In the end, the early inefficiencies are worth it.

Lack of equity

Argument

The extreme power imbalance and higher technical sophistication of private project developers and intermediaries often lead to opaque and unfair crediting agreements that mistreat local nature stewards. The lack of transparency in many environmental markets is a feature, not a bug. The only problem is that this feature is designed to enrich the intermediaries at the expense of Indigenous Peoples and local communities.

Additionally, most project developers and intermediaries don’t have the ability to achieve successful conservation projects in the first place. Many biodiversity conservation projects take place in remote areas with a weak rule of law, unclear land rights, and lack of institutional capacity. The developers and intermediaries, usually from the Global North, often cannot fully understand the cultural context they operate in. That is especially true for for-profit enterprises, where capital return time frames are shorter than the time it can take to build trust.

Counterargument

Once again, this argument is built on the worst possible unintended consequences of biodiversity credits. Under high integrity markets, such abuse of power would never be possible. Quite the opposite - transparency, fairness and empowerment of Indigenous Peoples and local communities are at the core of this market. The important part is ensuring that credit schemes and projects keep up their end of the bargain.

It’s true that it can be more difficult for industrialized players to relate and culturally connect to locals in the project area. Ideally, many of these projects would be (co-)led by these communities themselves. Of course, we still have a lot of work to do here. However, the access to finance, technology and stronger institutional capacity that the industrialized project developers have can also help to ensure nature and social outcomes at scale, if wielded correctly. Again, it all goes back to credit scheme and project design. If designed well, none of these challenges should be a deal-breaker.

Financialization of nature

Argument

Putting a price on nature is wrong on multiple levels. Not only does it legitimize nature destruction, but it also dishonors the complexity and value of nature. We cannot possibly quantify its value and whatever value we come up with is bound to be too low. By putting a number on nature, we are implicitly normalizing the economic decisions that destroy it. We’re normalizing the “that’s just how it works” justification by commodifying nature.

Also, since there is no standard definition of biodiversity, we can’t put it into a unit. Other environmental markets are based on commodities - clearly defined interchangeable units. We physically cannot commodify biodiversity.

Counterargument

The fear of financializing nature is emotional and understandable. However, this point of view ignores the fact that nature has already been financialized for a long time. The financialized value of intact nature is usually around 0. The economically valuable products of nature (natural capital and ecosystem services) are highly prized and used. The problem is, they just usually aren’t paid for. That’s why most forest owners aren’t compensated for preserving their forests - the local organizations just use these ecosystem services for free. Biodiversity credits can be one way to reward such landowners. Obviously, the social cost (& value) of nature is larger than any company is prepared to pay now. But it is better than the status quo.

Additionally, many biodiversity credit initiatives are not trying to value nature. They’re just trying to value the work required to protect and restore ecosystems. That is very different from just simplifying nature into a number.

Parting thoughts

If you made it that far, congratulations. Where does it all leave us though?

But first, a late little disclaimer: most of these arguments focus on the best and worst possible scenarios. They make it seem black and white. In reality, as always, it’s a sliding scale - few people subscribe to every extreme positive or negative argument. Those who do might be in trouble. As Naval Ravikant says, “You can approximate how independent of a thinker you are by noticing how neatly your political beliefs line up with those of your party.” Same applies here.

Different visions of the world

For some, biodiversity credits is the tool that will finally allow us to properly measure and systemically value nature with fairness. For others, it’s the newest neoliberal scheme to take from the vulnerable under the guise of environmental justice.

Why are these extremes so diametrically opposed though? Both sides are full of well-intentioned earnest people. So why? I think the answer is the different visions of how life should look like. Some believe that markets should rule everything. Others believe that governments should govern all. And there are also people who believe in a happy medium. That’s why you have full-stack financialization, complete market-based scheme boycott and outcome-based philanthropy as the main competing biodiversity credit end states (I wrote a bit more about it here).

You could even divide it into pro-system and anti-system. Or pro-capitalism and anti-capitalism. Some people accept the current set of rules and build on top of it. Others, usually indirectly, want to tear the current system down. Just think about how many market-based criticisms of biodiversity credits apply to other markets.

Ironically, both extremes operate under the “how life should look like” and not the “how life is” rules. The middle is more pragmatic.

And speaking of pragmatism, here are a couple of personal beliefs that calcified over these two years:

Unless the current system crumbles, economic growth will remain the priority of nations.

To grow, economies must produce and consume more goods. This is crucial for the material well-being of people (unless you live in a surplus economy, where overconsumption is the default).

Production and consumption of goods inevitably require natural resources.

The only thing that will actually make governments move is global ecosystem collapse.

And, maybe most importantly, people *want* to live materially better. That comes with higher consumption.

Now, there are a bunch of things we can do to minimize our environmental impacts. We can rewire and improve our systems (e.g. GDP is simply not a great human well-being tracker). But unless we acknowledge the inherent human desire to have more, no solution will stick. There are folks on both sides of biodiversity credits that acknowledge that. I hope they work together more.

On criticism

This piece made me realize how much easier it is to criticize. Poking holes is so effortless, especially in something new. Personally, I find it way easier to fall into the “everything is wrong” camp. The piece also helped me build more respect for the people “doing” stuff though. Even if it’s the wrong solution. Even if it will fail. This way of life has more hope - it’s brighter.

Speaking of hope, mine is that these very valid arguments against the biodiversity credit markets are not ignored. My hope is that they become opportunities for the markets to improve.

Acknowledgements

Although this topic has been simmering for a very long time, it wouldn’t have been as complete without many conversations with fellow industry peers and some specific knowledge sources:

Byron Swift’s commentary on why biodiversity credits cannot work

IAPB's (International Advisory Panel on Biodiversity Credits) framework for high integrity biodiversity credit markets

EPIC’s (Environmental Policy Innovation Center) paper on building a thriving biodiversity credit market

Frederic Hache’s thinking

Samuel Sinclair’s thinking

Sophus zu Ermgassen’s thinking

I’m sure I’m forgetting others. Thank you all.

p.s. thank you Morrison Mast for giving me the final push to get this idea out of the back-burner (& many others who shared their thoughts on this topic).

This article is gold worthy !! I will take all the time today reading it in every detail. But already the first glimpse is 👏👏